Develop an investment strategy

Frequently asked questions about rebalancing

Once you’ve selected an asset allocation tailored to fit your own time horizon and risk tolerance, you’ll want to stay on track. Rebalancing can help you stick to your plan.

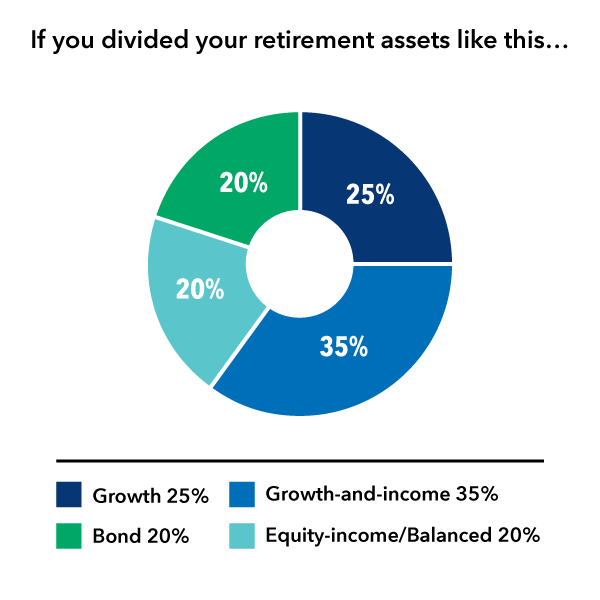

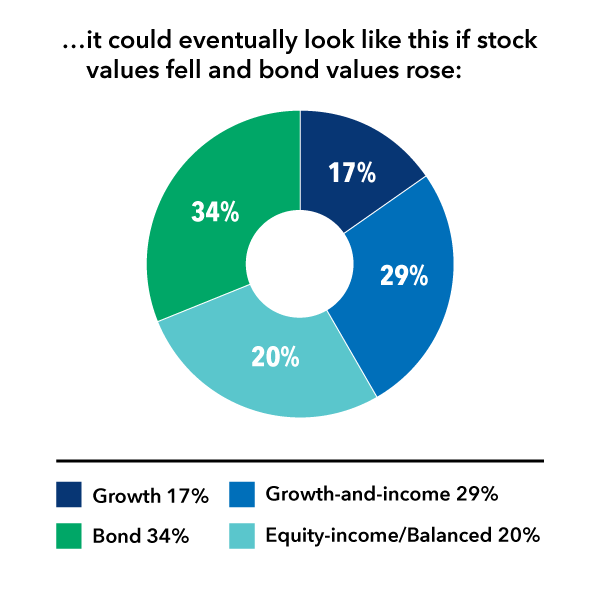

Your investments will gain and lose value as the market rises and falls. Because some investments will grow faster than others, you may need to move money from one investment to another in order to maintain the same asset allocation percentages you originally chose. See the example below.

These charts are for illustrative purposes only. The hypothetical examples are not intended to show the performance of any particular investment. Your results will be different.

In this example, to get back to your original allocation, you’d need to move some money from your bond funds into growth and growth-and-income funds. That’s rebalancing.

If you’re happy with your investment strategy, you’ll want to make sure the proportions of funds in your portfolio stay the same. If your allocation has shifted over time, you may want to adjust it to stay on your original course.

Remember, your decision to rebalance should be based on your long-term investment strategy, not on market results on a certain day. Rebalancing is not setting out on a new investment strategy. Rather, it is a way to stay committed to your original strategy.

Many experts suggest that you should consider rebalancing if the funds in your portfolio have strayed more than 5% to 10% from your original allocation, as illustrated in the pie charts above.

It’s a good idea to review your asset allocation at least once a year. Many investors choose an easy date to remember — such as birthdays or New Year’s — as their annual portfolio checkup date. If the markets are changing significantly, you may want to rebalance quarterly.

Before you rebalance, ask yourself if your investment objectives, time horizon or personal circumstances have changed substantially. Your investment mix should always accurately reflect your current needs, goals and plans.

It’s a simple three-step process:

- Review your original investment allocation you selected at enrollment.

- Check your current asset allocation — in your quarterly or year-end statements or on this website (if available) — to see if your fund proportions have shifted.

- If you need to rebalance, transfer money from mutual funds that have grown to be a larger percentage of your portfolio than you had originally chosen to funds that have decreased. This transaction is also known as an exchange. Your goal, if appropriate, is to return to your original allocation percentages.

Some plans offer a rebalancing option that automatically returns your investments to your original allocation. You may be able to rebalance your investments over the phone or through online account access. Check with your employer.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses. This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

American Funds Distributors, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.