Why participate in a salary deferral plan?

A salary deferral plan can help you prepare for retirement beyond Social Security. Here are three reasons to consider participating in your employer's plan:

Everybody loves a tax break

There are two basic types of employee retirement plan contributions that you can elect to have automatically deducted from your paycheck, each offering a different way to get a tax benefit.

- Traditional (pre-tax) contributions: You’re getting a tax break up front with traditional contributions because the money going into your account has not been taxed. By postponing taxes until you take withdrawals, you have more money working for you.

- Roth contributions: Made with money that has been taxed and won't be taxed again. Additionally, earnings are tax- and penalty-free for qualified distributions.*

In addition, retirement plan earnings aren’t taxed every year, so you could benefit from having more money in your account growing through compounding. Check with your employer to find out which contribution types your plan offers.

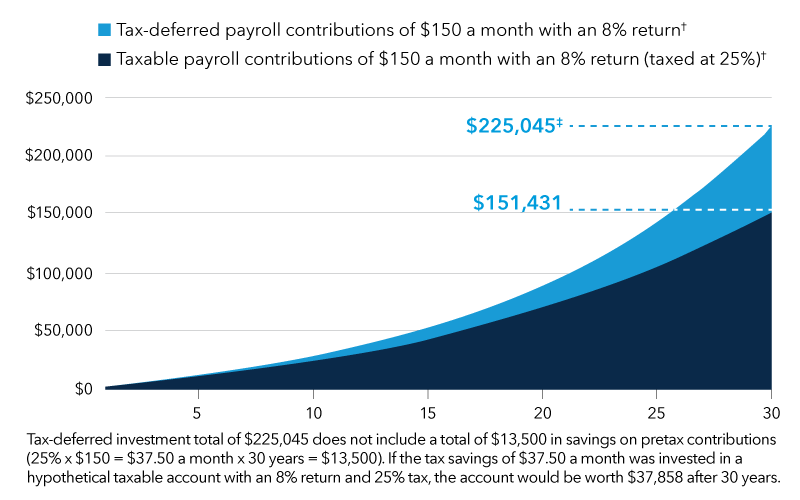

The chart below shows the hypothetical growth over 30 years of traditional, tax-deferred payroll contributions compared with taxable payroll contributions.

The tax-deferred advantage of traditional contributions

† The example assumes an 8% average annual total return (compounded monthly) and does not represent the results of any specific investment. Your investment experience will differ. Results for the taxable investment assume 25% in taxes is paid from the account each month, estimated in this example by reducing the 8% growth rate by 25% (so a 6% growth rate is applied). Lower maximum tax rates on long-term capital gains and qualified dividends could make the taxable investment return higher, thus reducing the difference between the two ending values shown. This chart does not address the impact of Roth after-tax contributions.

‡ The money you take out of a tax-deferred retirement plan account is subject to ordinary income taxes at the time of withdrawal and, if applicable, a 10% early withdrawal federal tax penalty. Withdrawing large lump sums may push you into a higher tax bracket. For example, withdrawing the $225,045 at a 33% tax rate would leave you with $150,030 after taxes. However, you might pay a lower tax rate if you withdraw smaller portions of your account balance over time, and the remaining balance would have the opportunity to grow tax deferred. Your actual tax rates may vary.

A program of regular investing does not guarantee a profit or protect against loss.

You wouldn’t turn down free money

Many companies offer matching funds as an incentive to encourage employees to contribute to their salary deferral accounts. If your employer offers to match your retirement contribution, take it. It’s as if your employer is paying you a bonus — and all you have to do is save in the plan. Contribute at least enough to get the full match. If the match is in company stock, think about diversifying the rest of your account. The match is part of your benefits package. Don’t walk away from it.

Social Security won’t be enough

If you plan to rely on Social Security to pay all your bills, your retirement dreams may need to be trimmed back. The rule of thumb is that Social Security probably represents only 40% of your retirement needs. According to the Social Security Administration, the estimated average monthly Social Security benefit for January 2023 was $1,827. Even with cost-of-living increases, this won’t buy the kind of retirement most Americans dream about. When you participate in your retirement plan, you take control of supplementing Social Security.

Visit the Social Security Administration website for more information about the retirement benefit you can expect.

* Withdrawals from Roth accounts are tax- and penalty-free if the account was established at least five years before, and if the participant is at least 59½ years old, has died or is disabled. For nonqualified distributions, earnings are taxable and may be subject to a 10% early withdrawal penalty.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses. This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

As of July 1, 2024, American Funds Distributors, Inc. was renamed Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.